Sunday thoughts: Big Lots and Bath & Body Works

Continuing to lean into consumer strength and buybacks

I plan to put a little capital to work next week in Big Lots (BIG) and Bath and Body Works (BBWI) as I continue to have strong faith in consumer demand and good management groups. Both companies to me could be beneficiaries of a market:

Assigning low expectations to omnichannel retail, as reflected by price

Discounting earnings expectations for companies it views as one time COVID beneficiaries

Let’s get into it.

BIG

Big Lots reported Q3 earnings Dec. 3 (Friday) and notched “record Thanksgiving and Black Friday sales”. Perhaps even more importantly, they gave strong guidance for next year and expect to see margins continue to improve:

Looking forward, we expect to post a new record sales year in 2022, and we have ever-increasing confidence that our key growth drivers under Operation North Star – materially growing merchandise productivity, accelerating new store growth, and continuing to ramp up our ecommerce capabilities – represent a huge white space opportunity for us. In addition, we expect to see gross margin expansion in 2022 driven by promotional and pricing optimization, the deployment of new planning capabilities, and favorable mix effects. As we look towards closing out 2021 and beginning a new year, we are primed, pumped and laser focused on being the best destination home discount store.

I want to highlight two things here - 1) extremely positive comments from management on the strength of the consumer and 2) the company’s insane buyback activity.

On the consumer - Big Lots CEO Bruce Thorn (who you’ll see tends to refer to the consumer as “she”) had the following to say:

In terms of customer trends, I'll tell you what, she's out there revenge shopping. As we mentioned in our opening remarks, our fourth quarter is off to a very good start. The largest Thanksgiving and Black Friday week in our company history and 10% 2-year comps through November. The customer is healthy. We're seeing her shopping earlier. In fact, we -- our research told us about 50% of Americans plan to shop earlier than Thanksgiving this year for the holiday season, and we're seeing all of that come true.

Thorn also does not see inflation stopping the consumer:

We're not seeing a pullback in consumer spending or customer spending as a result of the inflation. Right now, we are actually seeing that the price increases that we've put through as a result of covering of costs that we're getting from input product and freight is being absorbed by the customer.

She wants the product, especially going in the fourth quarter, she knows that she needs to shop early. We're not seeing that resistance.

BIG is putting its money where its mouth is, betting on the consumer via adding 50 new stores next year (will be back half loaded with 15 in 1H 22 and 35 in second half). BIG is growing.

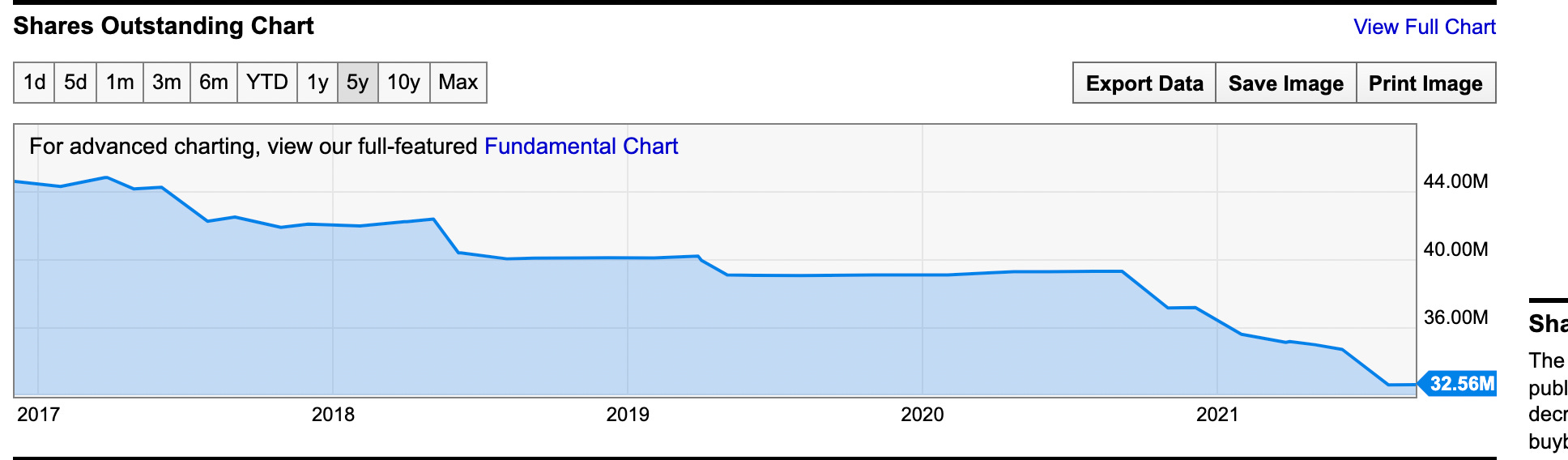

If the capex bump from a program like this scares you, keep in mind BIG has been a massive buyer of its own shares. The share count was 31.7mm as of 12/3; if we rewind to 2/1/2020, it was 39.2mm - this is a 19% decrease in share count in <2 years. Courtesy of Y Charts, here’s the company’s shares outstanding history over the last 5 years:

In just the last quarter alone, the company bought back 2mm shares at an average cost of $47.43. The stock is trading below this price as well as the $53.49 average since Aug. 2020. I fully expect the company to continue aggressive buybacks given their positive outlook and the bargain they’re getting on the stock relative to historical purchases.

I think BIG stock will work if you look at the math on buybacks and organic growth from new stores. Relative to earnings, the stock continues to trade cheap relative to historical levels:

BBWI

For a refresher on Bath & Body Works, I highly recommend Diligent Dollar’s post on them as well as my podcast with him from a few weeks back. The company reported Q3 earnings Nov. 17 and while Q4 guidance came in a little short of guidance ($2.10-$2.25 versus ~$2.39 on analyst community), they beat on Q3 and I think it’s possible with buybacks (guidance doesn’t take into account) and a little holiday magic they could come in close to the expected $2.39.

Like BIG, the commentary here was strong and repurchase activity continues to impress. BBWI has been able to increase prices without consumers exiting:

Let me add my own commentary here - I was at the Bath & Body Works at Wrentham Outlets yesterday and it was one of the only stores with a line and most people in there were purchasing three-wick candles for $10.95.

The employee at the door told me this line was nothing compared to what they saw Black Friday. Seems to support management’s claim pricing changes aren’t impacting demand at all.

On the scuttlebutt side, would also add here the refresh the company did for Q4 looks great and they are very much leaning into candles, scents, hand sanitizer and self-care category items as “add-on” gifts for the holiday season (notice the pre-packaged gift baskets):

Finally, just like BIG, repurchases are strong here:

The company currently has a $19.3bn market cap, meaning the $365mm post spin-off last quarter was ~2% of the float.

Overall, I’m very comfortable adding to positions in both names because:

Inflationary / supply chain pressures do not appear to be impacting sales at either company

Strong balance sheets / shareholder focused management groups allow each to return cash to me in the form of buybacks, meaning I’m getting more ownership in the company without moving a finger

Interestingly, BIG was up ~5% Friday on earnings and BBWI has not participated in the market drawdown of the last few days. The market may be signaling readiness to increase expectations for both.