Total Site Solutions - data center upside with customer concentration risk

Walking through Dell, sales and margin potential

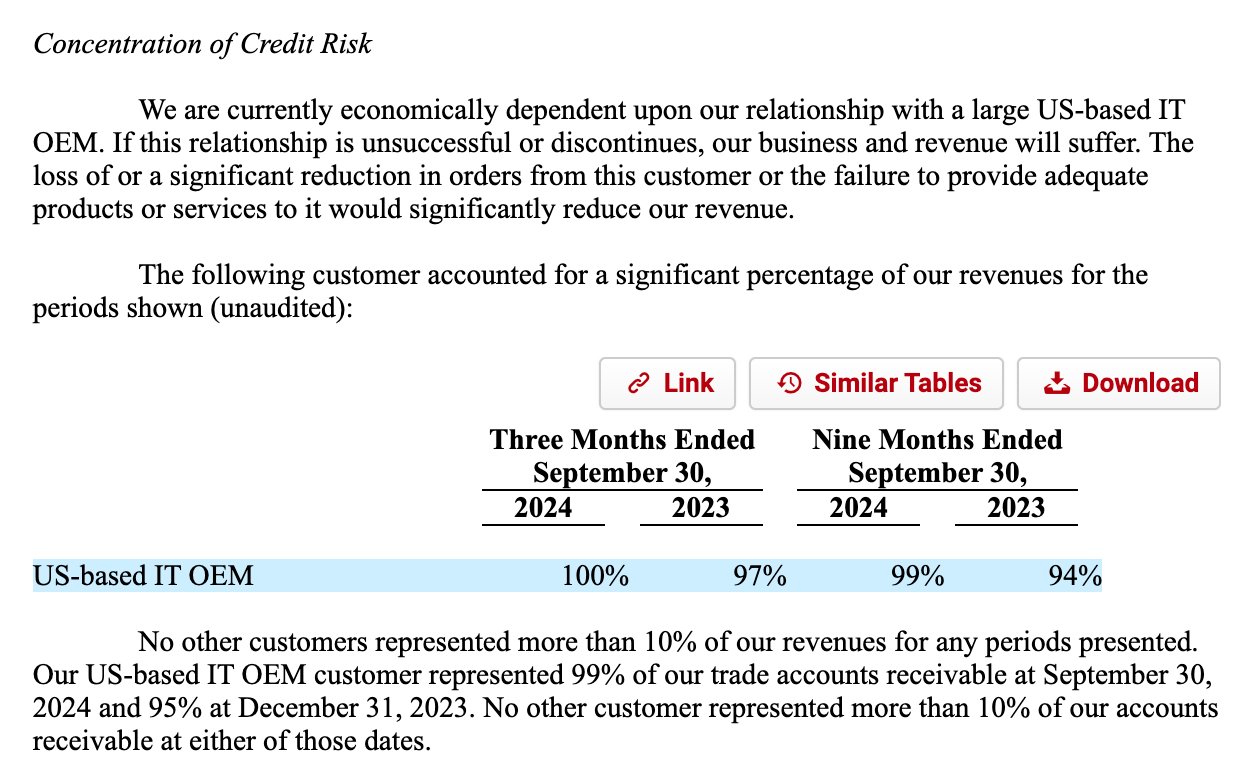

I almost put Total Site Solutions (TSSI) in the “too hard” pile. The company’s revenue right now is nearly 100% derived from Dell and ~80% from asset procurement for data centers. Asset procurement is a low margin business (gross margins around 4%).

From the last 10-Q:

However, I think there are mitigants to the Dell relationship risk and thin margins. I like the upside from many AI tailwinds and the potential to learn more about data centers. First, let’s walk through a little company history.

The last quarter and some history

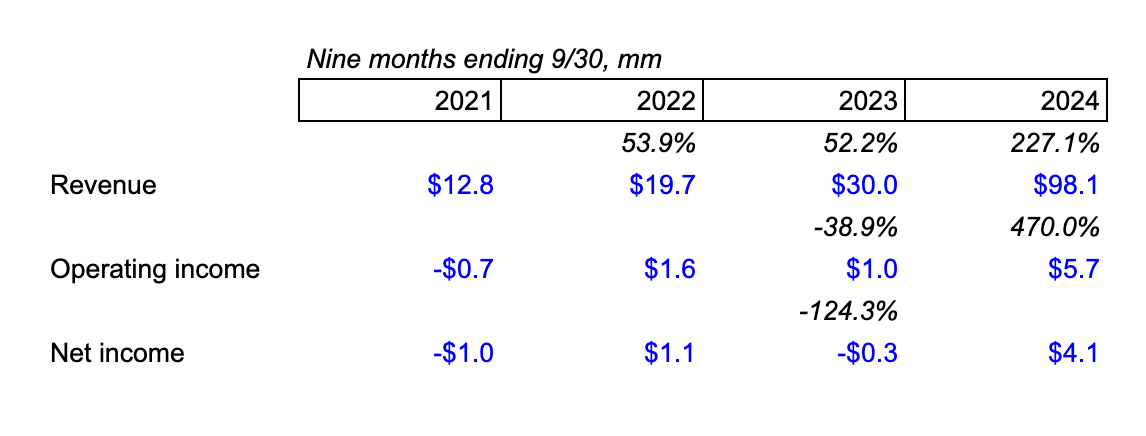

Total Site is very much a beneficiary of being an AI picks and shovels name that is coming off a massive quarter. The stock was uplisted to the NASDAQ in Nov. 24 from OTCQB (basically, the pinksheets). In the last 365 days, it has run from an ~$8.2m to $295m market cap (yes, this is a 3,500%+ gain). However, fundamentals during that time have also taken off:

The first nine months of the year have 4xed+ any compared period on growth. The last quarter specifically has stood out as in Q3 sales were $70m versus $8m in the prior year with $3.8m of operating income versus $0.7m in the prior year Q3. There are reasons to believe in future growth ahead and the stock has re-rated.

The new management team deserves credit for some of the success; CEO Darryll Dewan has been at the company for a little over two years (the prior CEO, Anthony Angelini, was there for 11 years) and the CFO Danny Chism has been there six months. Much of 2023 per the company was focused on streamlining operations and improving the relationship with Dell. These efforts clearly paid off, as in Sept. 23 Dell named Total Site its First Choice Partner Award.

The company was founded in 1991 and became publicly traded through a SPAC led by Fortress America in 2006. Dell was listed as a new customer in a 2007 press release so the relationship is at least 17+ years old.

What does TSS do?

Total Site handles the integration and deployment of data center infrastructure. While most of the revenue comes from Procurement, they record higher margin revenue in Facilities Management and Systems Integrations. Some quick explanations below:

Procurement - Procurement is ~80% of sales and comes mainly from ~4% margin transactions where TSS buys hardware on behalf of Dell or another customer and pockets the difference when Dell buys it from them. TSS may modify or “transform” the product to make it appropriate for its use case (ex. placing in a data center). The company calls these “gross deals” in their accounting. Sometimes the company will act as an agent between supplier and their customer and collect a commission when the supplier delivers - these are called “net deals”.

Facilities Management - The company in this business segment does project management and engineering services for data center development. These services include load testing, subcontractor vetting, heating and cooling management and a range of other services. The project manager from TSS will stay with a project until completion and oversees all of TSS’s involvement in building the data center. Maintenance of facilities is part of this business segment so some of the revenue is recurring. Gross margins are 37% for facilities management per the last Q, but are higher for modular data centers (more on this soon).

Systems Integrations - TSS is responsible for integrating hardware and software in data center deployments. Again from the last Q, systems integrations gross margins are 45%.

Importantly, the company has talked about Modular Data Centers (MDCs) on recent calls as a key part of future facilities management and other revenue. MDCs are assembled in advance (they can be put in a shipping container) and typically faster to install than traditional data centers (good overview of MDCs v. traditional here). TSS has assembled and deployed over 500 MDC deployments and is an area they’re excited about:

We see the potential for more robust growth in this segment in 12 to 18 months as more medium and large enterprise clients consider using modular data centers as a cost-efficient means to harness the power of AI technology without the need to build out full data centers with all the requisite cooling capacity.

…Shifting to a quick look at our Facilities Management activities, primarily for our modular data center, or MDCs, as we refer to it, we continue to experience moderate overall growth with the segment's revenue up 8% this quarter. This is a more predictable business line for us, with healthy gross margins typically north of 50%. I've previously highlighted a few challenges in this business, primarily from rapidly increasing compute density and evolving cooling requirements. We believe the expanding adoption of AI-enabled technology will drive incremental demand for MDCs and produce revenue in 2025 and beyond, due primarily to long lead times for the new modular data centers. Whether this materializes as predicted remains to be seen.

The 50% gross margin here is well north of the 37% overall gross margin on facilities management; if TSS can move more of this business line to MDCs, we should see margins go up.

The company’s demand mainly comes from Dell for all these services. Dell has also provided loans to the business. There is a good amount of commentary in the last few transcripts that suggest they’re trying to diversify away from Dell, and I thought this call-out in the 10-K was worth excerpting:

A key part of our selling strategy is entering into master service agreements with multiple partners and co-selling our range of services to our partners’ end-user customers, leveraging their customer relationships and broadening the scope of potential customers for us. Our go-to-market approach formerly relied on business generated by one major OEM customer. While this business was and remains valued, it has been difficult to forecast resulting in inconsistent and fluctuating quarterly results. This approach relied on expertise in information technology hardware systems, energy consumption, real estate matters, and facilities planning and operation from this primary demand source. This marketing approach allowed the end–user customer to contract for comprehensive facilities services or to contract separately for each project phase such as integration or fulfillment services.

Our updated go-to-market strategy is designed to capitalize on our investment in direct selling personnel and leveraging our OEM partner’s capabilities at the same time. Our ability to be involved in sales engagements earlier in the cycle and with end-users will allow us to positively impact demand and provide greater visibility into the integration schedules and future pipeline. This impacts our ability to better manage personnel schedules and ultimately optimize our production capacity.

The next few years

AI demand causing an inflection in the company’s strategy and results is the upside here. For most of TSS’s history, data center demand was not driven by AI and the design of data centers was not much of a moving target compared to now. The needs of modern data centers seems to change every day now. As an example, I liked this write-up from Semi Analysis on the new needs for cooling systems in data centers - Direct Liquid Cooling is something Total Site can help with. DLC to me is one of many types of assets that are changing before our eyes and will make asset procurement and deploying / integrating those assets even more important. Semi Analysis writes:

Of the key datacenter systems, Cooling is arguably the area that is evolving at the fastest pace, presents the steepest learning curve and carries the execution risk for datacenter operators. With large-scale projects commonly requiring billions in capital expenditure, the stakes are extremely high. Rapid advancement in datacenter requirements also amplifies the risk of developing assets that could become obsolete quickly.

Total Site has competitors - Super Micro (SMCI) is the leader in the market - but often works directly with them. Again, the data center in the AI era is becoming so complex and fragmented it suggests to me TSS will have plenty of market to go after for years. From the last 10-K:

The mission-critical information technology solutions market is large, fragmented, and highly competitive. We compete for contracts based on the strength of our customer relationships, successful past performance, significant technical expertise, specialized knowledge, and broad service offerings. Our strength lies in our ability to deliver quality solutions on time and with high quality at a competitive price. These solutions can be complex or simple. We have gained traction by providing complex AI solutions utilizing GPU and advanced thermal management technology. We often compete against channel re-sellers and divisions of large information technology service and equipment providers. In some cases, because of diverse requirements, we collaborate with these and other competitors for projects. We respect competition in the information technology services sector, and we embrace what we need to do to compete and win to continue to increase in the future.

The company lists Walmart, Microsoft and Bank of America in its last investor presentation (obviously these are very small money compared to Dell based on the quarterly filing). One account on X noted Total Site has a job posting in Boydton, VA which is where Azure has data centers for their US-East region.

Pricing the upside

On a trailing earnings basis, I don’t think TSS’s valuation is ridiculous when you account for growth (assuming you believe future earnings can grow, which I do).

Just using the last nine months of earnings, TSS trades 73x; the last quarter was $2.6m of net income, so if they repeat Q3 in Q4 this trades ~45x LTM. Given that revenue just grew 689% y/y and operating income was up 431%, I think 45x P/E actually is not expensive. If you think Q3 is a good proxy where they did $0.10 of EPS, I don’t think it’s out of the question to see $1-$2 of earnings in 2026 or 2027; the assumption here is they can get to ~$500m+ of sales with 5% net income margins. Q3 NI margin was 4.1% - I think facilities and systems integration can come up in future, especially if modular data centers gain popularity. 5% margin on $500m of sales is $25m of earnings ($1 of EPS at 25m shares). I think in an upside scenario AI is still outperforming most industries on a growth basis in 2-3 years and it’s fair to get a premium multiple - assume 25m shares and you get to a $25 stock price at 25x ($625m market cap). So, a double in <3 years seems more than realistic to me.

I also think we could see higher sustained growth and multiple expansion if TSS proves they can move beyond the Dell relationship.

I think even if TSS does not diversify off Dell, there are ways to win here. The current CEO worked at Dell for a decade. Both companies are headquartered in Round Rock and a few miles away from each other. Based on the award they just won, the relationship seems to be in a good place and last call an analyst even asked if an acquisition was a possibility:

A couple final notes here:

The company just announced a $20m credit facility to relocate its headquarters and build a new factory through a 213K square foot lease in Georgetown, TX. They have specific power arrangements with the city of Georgetown because some of the server rack work they’re doing is so power intensive. TSS also announced a shelf registration in that same release which does suggest they could be doing an equity raise (a little concerning, but if they have the return on capital math working, could make sense).

From the last proxy (4/30/24) - the equity is 17% owned by Peter Woodward, who is the Chairman of the Board (has been chair since 2012) and president of MWH Capital Management (microcap fund). The former CFO owns 4% and the current CEO owns 3%. Glen Ikeda owns 7%; interestingly, looks like he gave the company a 300K loan in 2017; it’s unclear to me to what extent he is involved today but is the second largest individual shareholder.

Overall, my biggest reservation with Total Site is that I’m incorrectly annualizing sales and earnings and projecting future growth when the last quarter represents a one time bump. Asset procurement is not a recurring revenue business, despite TSS management saying last quarter is representative of the next few quarters. Procurement margins may get squeezed from the already thin 4% of last quarter. I may also be incorrectly viewing TSS’s moat / position in the data center lifecycle. I’m ready to be wrong on this one but like having exposure to a high-upside data center name that appears to be at an inflection point.