Triton's decreasing cost of debt

Right side of balance sheet and strong lease environment spell ATHs

Triton briefly touched all-time highs yesterday in part because of its announcement of new senior unsecured ten year debt at 3.25% (issued a little below par) that will pay down its revolver:

[The company] priced a public offering of $600 million aggregate principal amount of 3.250% Senior Notes due 2032 (the “Notes”) at an offering price of 99.600% of the principal amount thereof. The Notes will be guaranteed on a senior unsecured basis by the Company. The offering is expected to close on January 19, 2022, subject to the satisfaction of customary closing conditions. The net proceeds from the offering are expected to be used to repay borrowings under the Company’s revolving credit facility.

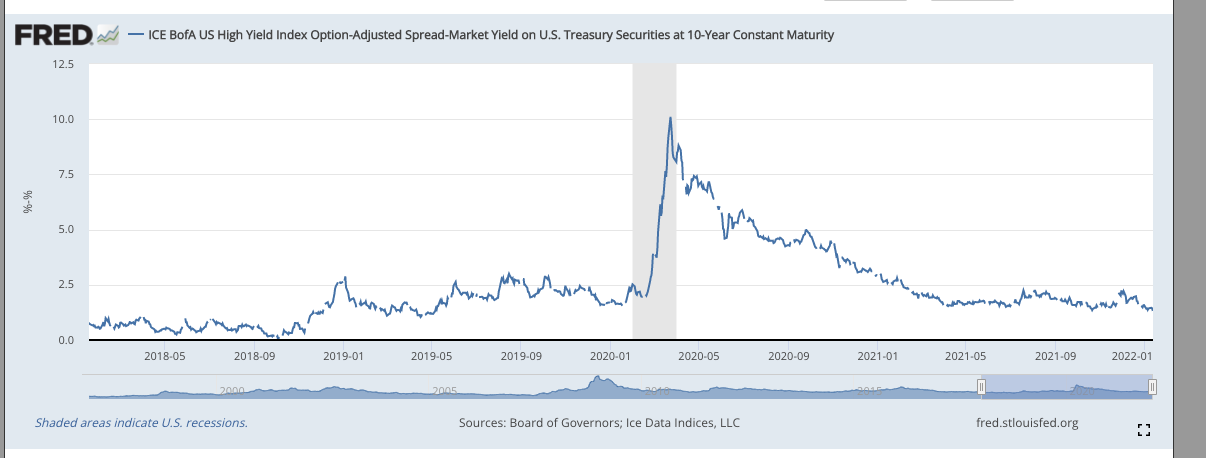

To get a sense of how cheap this is, consider that the 10 year currently is at 1.72%, so TRTN priced at T + 153bps. In November 2018, the 10 year treasury traded to 3.20%.

This is fixed rate debt and protects Triton from rate increases going forward (although I don’t see that being as large an issue as some people think). I think the company’s timing was close to perfect considering high yield spreads have majorly tightened (note TRTN is a BBB- issuer that was upgraded in Oct. 2021 by Fitch and S&P, so is technically on the cusp of investment grade):

More importantly, this lowers the company’s long-term cost of capital and continues a trend of Triton decreasing its cost of debt. I think it’s informative to look a bit at the company history. Here is where TRTN stood with debt costs in 2019 per their annual report:

Now let’s look at 2020:

Finally, let’s look at Q3 2021:

It’s worth it to do some quick comparisons over time. Some fast facts:

On ABS (asset-backed security) notes, Triton’s weighted avg. interest rate has gone from 3.69% to 1.98% in two years

Triton’s revolver debt cost went from 3.45% to 1.62% (also all due to LIBOR decreasing, but still)

The former has been possible through an ABS market that has massively tightened:

Let’s rewind back to March 2018 - Triton issued $400m+ of Class A ABS notes at ~4%

Triton in March 2021 issued ~$700mm of fixed rate Class A ABS notes at ~1.9%

The latter also is a result of a low rate market and the company’s own initiative:

The revolver also changed from secured to unsecured

Some of you reading this may be thinking “Hold on a second - 3.25% is higher than the ABS and the revolver". This is true, but consider that senior unsecured debt is a different type of financing than either of those things and has its own advantages:

Unlike ABS, senior unsecured debt for Triton has bullet maturities and doesn’t amortize till the very end, meaning Triton’s cash payments for the next ten years don’t include principal like ABS

Unlike ABS, Triton doesn’t have to pledge container assets, where it generally got 80% of the value of each pledged container in debt. Triton’s ability to raise ABS requires them to either contribute existing or buy new containers into the ABS pool. We know Triton wants to be disciplined with buying containers to avoid flooding the market, so senior unsecured allows them to be selective because they receive cash with no commitment to buy containers

Unlike a revolver, Triton’s senior unsecured debt doesn’t float and isn’t subject to floating rate risk

Unlike a revolver, Triton’s senior unsecured debt has a ten year maturity

I continue to believe this should have a material impact on free cash flow. The company as of Q3 2021 had $8.3bn of debt. If you conservatively say its cost of debt is 1% lower than it historically has been, that is $83mm annual of interest saving. From an earnings perspective, let’s say TRTN does $700mm this year - that is an 11% increase from cost of debt alone.

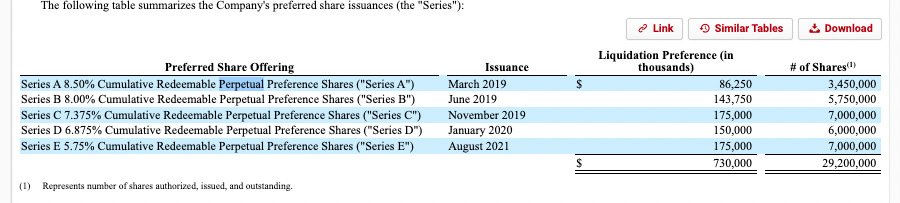

What gets me excited going forward is Triton has expensive preferred stock it can take out with cheaper debt. In FY20, the company paid $41mm in preferred dividends. Here’s what those shares look like:

Some of these may have prepayment guards, but long-term retiring $730mm of preferred shares with debt should be easy for them. Throw on that $41mm of cost savings from not having to pay those preferred dividends and we’re now talking about $124mm of cost savings a year. On a per share basis, TRTN had 66.7mm shares outstanding at the end of Q3, so that’s $1.85 per share. Sure, that may seem like only 2.8% on a $65 stock, but remember the company can allocate that cash any way it wants. We could easily see the dividend increase or the company ramp up container purchases if supply chain issues and a strong economy continue.

I’ll end this post with my favorite slide from TRTN’s Investor Day presentation. Think about this slide in the context of this post and the $1.85+ of distributable FCF. The company already has a ton of dry powder to award shareholders when it sees fit; the debt cost savings are the cherry on top: