Bath & Body Works - yesterday's selloff is buying opp

Hard to make sense of what market is thinking here

Bath and Body Works (BBWI) updated guidance yesterday and communicated it will land on the high end of its estimates for Q4:

The company currently expects that fourth quarter earnings per share will be at the high end of its previous guidance of $2.10 to $2.25, compared to earnings per share from continuing operations of $1.96 in 2020.

The company expects fourth quarter sales at the high end of its previous guidance for a mid- to high-single digit percent increase compared to 2020.

The company will report fourth quarter earnings on Feb. 23, 2022.

Andrew Meslow, Chief Executive Officer, said “We are very pleased with our Holiday results, which exceeded our expectations, driven by strong customer response to our Holiday assortment...”

I wrote about the company in early December and noted 1) I went to the Wrentham outlet location and the store was absolutely packed in the first weekend of December and 2) the market was already disappointed with Q4 guidance:

The company reported Q3 earnings Nov. 17 and while Q4 guidance came in a little short of guidance ($2.10-$2.25 versus ~$2.39 on analyst community), they beat on Q3 and I think it’s possible with buybacks (guidance doesn’t take into account) and a little holiday magic they could come in close to the expected $2.39.

So now we know they’re going to hit the high end of guidance, and per this article expectations have now changed to $2.27. I am unsure why the stock fell 6.4% yesterday and added to my position, as I have high conviction in the strength of the company’s brand (candles + scents that sell like hotcakes even with price increases), its ability to maintain best in class margins (low-mid 20s on operating margin long-term per management) and management’s capital allocation strategy which rewards shareholders (emphasis on buybacks).

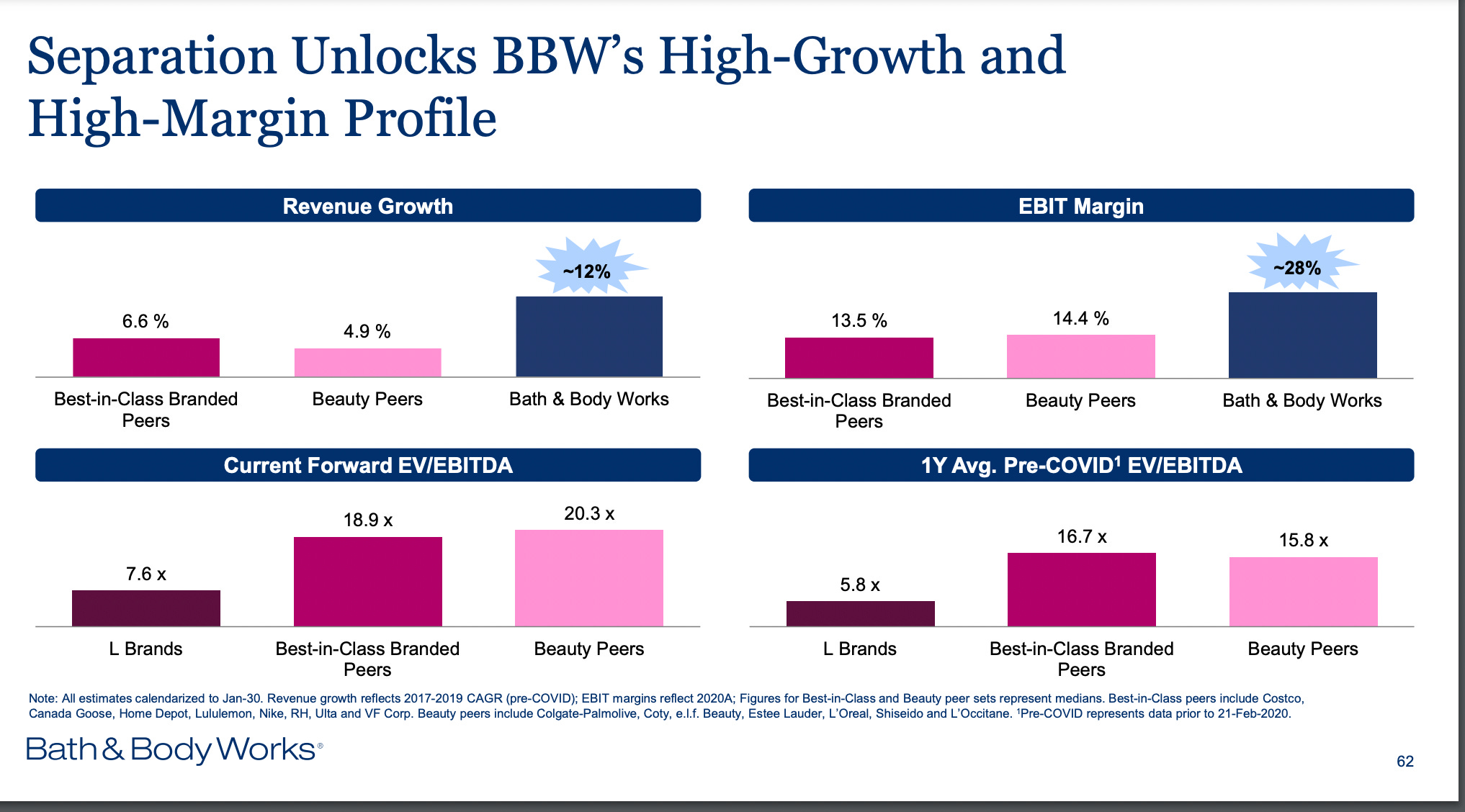

On valuation, the company’s enterprise value is now sitting at ~$19.5bn ($16bn market cap + $4.85bn debt -$1.4bn cash) versus long-term EBIT I think can be $2bn+ ($6.4bn 2020 sales, say that grows to $10bn over time and apply 20% margins, company said in its investor presentation to expect high teens to low twenties revenue growth). The $2bn in EBIT I think is about $2.5bn in EBITDA (company has done $500mm+ in depreciation the last few years). BBWI points out its peers trade at anywhere from 18-20x forward EBITDA (note the company used to be part of L Brands before going independent in the middle of 2021):

At $2.5bn of EBITDA, the stock looks like it could reasonably double from here:

Zooming out, I think the company has that magic formula I look for in companies I want to own forever - strong unit economics and a long runway, in this case in the form of a big international market they’ve shown they can grow in:

I continue to believe the company deserves a premium multiple based on these factors and am not concerned with an overreaction to what I thought was a positive guide yesterday.