BetMGM raises revenue and EBITDA guide

Raised guidance makes $500m long-term EBITDA guide look possible

MGM is a buyback machine (see my full write-up here) with stable earnings power (hotels, slots) and a growth asset in BetMGM I think the market hasn’t fully appreciated yet. As a reminder, BetMGM is a 50-50 joint venture between MGM and Entain formed in 2018. The prior update I wrote about in April was notable because EBITDA went from a $132m loss in the same quarter in 24’ to a $22m gain in Q1. BetMGM on 6/16 guided to $100m of EBITDA (previous was just EBITDA positive) for the year and reiterated $500m in EBITDA “in the coming years”. Revenue guidance also increased by $200m on the low end. From the release:

This continued strength provides BetMGM increased confidence in its performance for 2025 and as a result BetMGM upgrades its guidance for FY 2025:

FY 2025 Net Revenue is now expected to be at least $2.6 billion (up from the previous guidance range of $2.4bn to $2.5bn)

FY 2025 EBITDA is now expected to be at least $100 million (up from the previous guidance to be EBITDA positive)

Reiteration of the expectation that Online Sports will be contribution positive for FY 2025, in addition to strong contribution2 from iGaming

BetMGM remains excited about the significant opportunities ahead. Its strengthened business, revised strategic approach, and performance momentum, further reinforce its confidence in future growth prospects and pathway to $500 million EBITDA in the coming years.

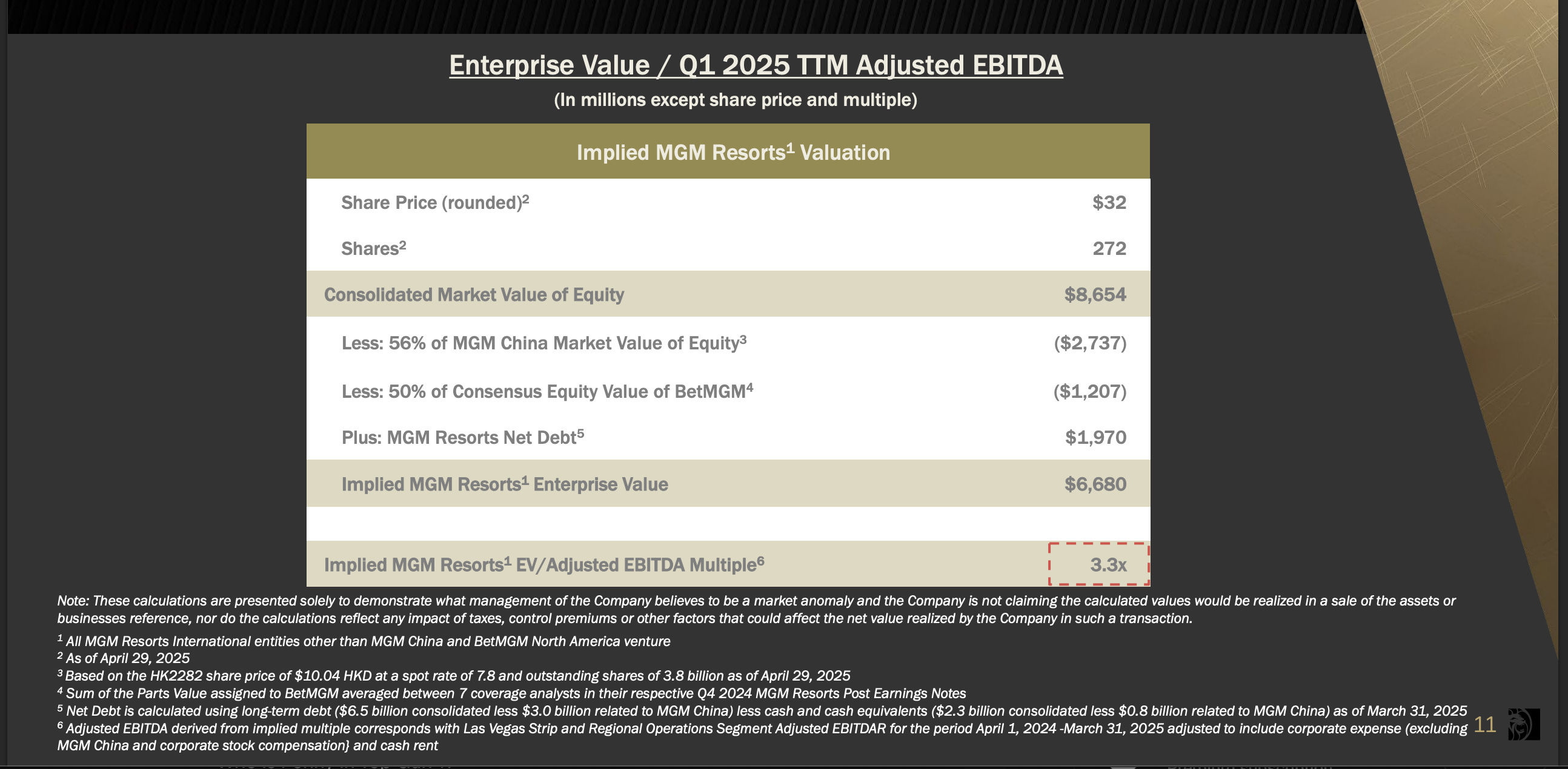

Entain and MGM were both up at one point 8% each on the announcement and I think the move up is well deserved. On an EBITDAR basis, MGM is doing about $2bn today so BetMGM if you believe the new EBITDA guidance could be a 10%+ contributor (MGM owns half so $250m long-term). From the last deck:

At ~$34 today and share count shrinking, I think expectations for MGM are very low.

I also think $500m of EBITDA if you zoom out 10+ years could prove low. New sports & other betting products and promotions are driving growth among existing players. The last quarter showed more player engagement rather than new player acquisition driving growth. In Q1, BetMGM revenue growth (+34%) and margins were up when average monthly actives were only up 6%:

When California and Texas go legal (may take till 2027-30+ to be clear), I think over time we’ll see first growth from player acquisition and then growth from increased betting. These states legalizing are no doubt baked into the $500m guide. However, given that we just saw BetMGM raise without any states legalizing since the end of Q1, I’m betting (pardon the pun) that the joint venture is realizing existing player value faster than expected.

Functionally, this might mean offering more same-game parlays on the app’s home screen or better personalized promotions over email / app notifications based on betting activity. AI is definitely a tailwind here as predictive and personalized features are faster and cheaper to develop now. Related, MGM’s hotel business may also be benefitting from AI. From the Q1 call:

Back to sports betting - I can’t watch a Celtics game now without the live moneyline and spread popping up every two minutes. The long-term trend is towards handle per player and active players going up for sports betting. We just saw EBITDA margins go from negative to positive for BetMGM this last year. Operating leverage is kicking in faster than originally forecasted.

One final thought here - in researching this post I was surprised to find that Entain’s CEO has already discussing spinning off BetMGM:

“So you know there is no real hurry for us or our partners to do further – to crystallize the value here. And then when we reach that point, that could open up further opportunities for us, so whether it’s through dividend, or whether we at some point could look at an IPO.”

This outcome would be a clean way for both Entain and MGM to exit the JV and not have to talk through capital allocation decisions like paying dividends. The IPO option I think would be especially interesting in 2028 or later if timed when Texas and/or California legalizes.

BetMGM reports Q2 on 7/29. If we keep seeing great results, I think the probability of an IPO rises.