Making the case for infinite duration bonds ($NOW, $TRTN)

How much should today's rate spike cause forever cash flows to re-rate?

Stocks are infinite duration bonds with uncertain coupons. You own all the cash flows and assets available after debtholders are paid forever. As a result, the “forever” or "terminal value” of a stock is:

(FCF * (1 + growth rate)) / (Discount rate - growth rate)

For zero growth rate stocks, this is:

FCF / discount rate

In February, I wrote about how as equity prices come down, you can start assuming lower and lower growth (in some cases, zero or negative) and still get your expected return using the terminal value formula:

I wrote a post in early July about interesting bond opportunities; while those opportunities have now become more attractive, I also think given a sufficiently long time horizon (let’s say 10+ years) it’s impossible to deny the case today for stocks.

Given that terminal value can be driven by current FCF yield or future growth rate, I’m going to bucket equity opportunities using those two drivers.

Attractive Future Growth Rate with 10y Like Current FCF Yield

There’s also the competition factor. Just looking at where we stand in the market, I’m sure there are investors who would prefer to sit out this market and relax in a 4.3% Treasury for a year or so. Sure, it’s not a big gain, but at least you don’t have to worry about the market’s frenetic volatility. It’s not for me, but I understand why some people would happily go for it. Who needs the headache?

If the 10y treasury were a stock right now and you were confident rates would never change and it traded at par, it would trade 25x free cash flow ($4 coupon on par of 100). A number of companies with growing equity “coupons” are trading 25x FCF or close to it (necessary disclaimer: before stock-based comp), including NOW 0.00%↑, MSFT 0.00%↑ , and GOOGL 0.00%↑ .

ServiceNow is a particular favorite of mine as I agree with management that we are in the early stages of a "workflow revolution". I think they have a sizeable growth runway ahead of them.

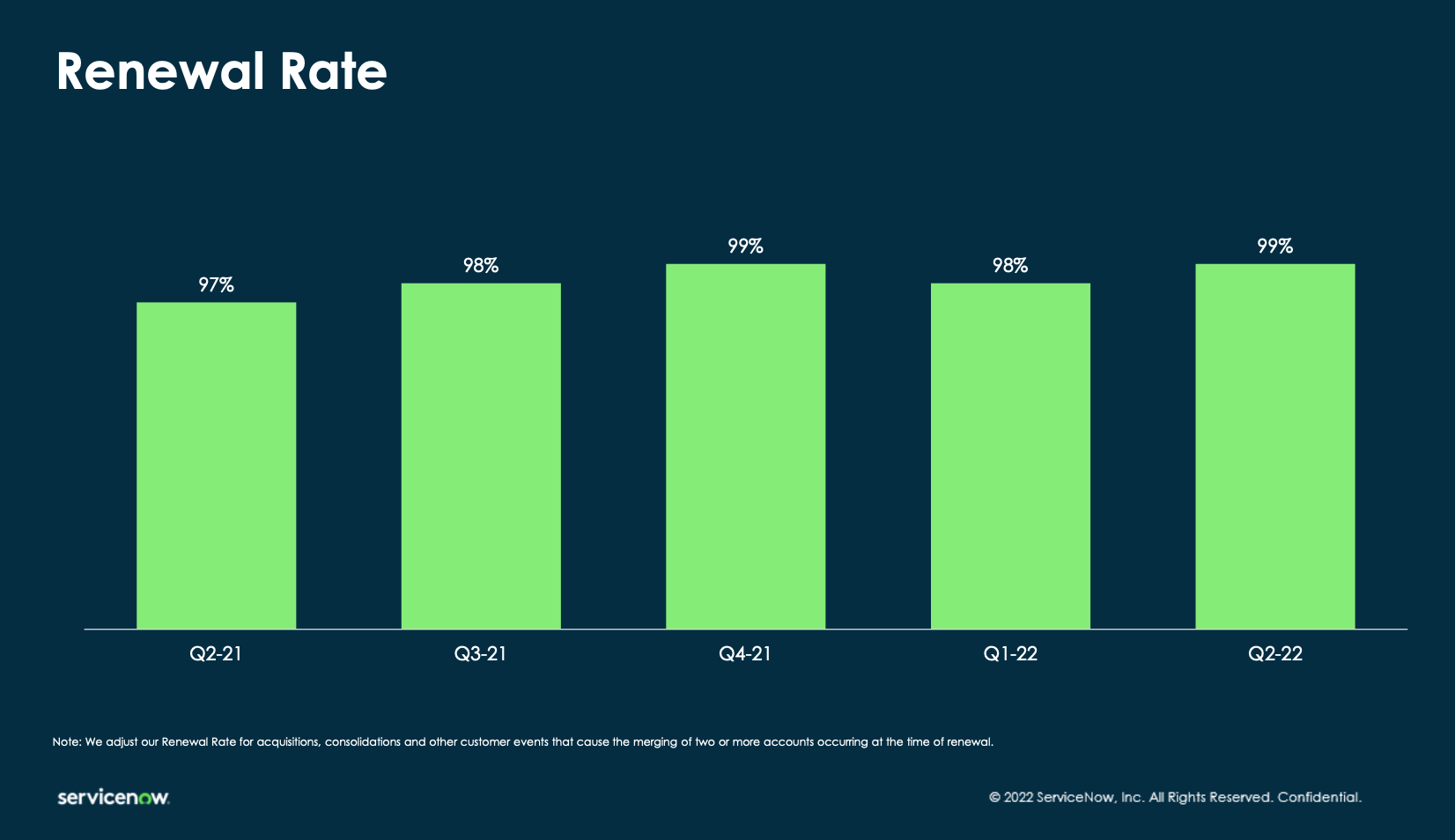

Existing cash flows are extremely stable, with contract renewal rates in the high 90s since the company went public (all sides to follow from this Q2 presentation).

Additionally, NOW does a great job growing revenues with existing customers. Customers they’ve had for a decade have more than doubled average contract value with NOW. From the Q2 presentation:

NOW was a rare “rule of 60” company in 2021, with 30% revenue growth and 32% FCF margins (equity dilution also has been <3% last several years). Most importantly on the growth side, NOW in its last investor day is projecting $16bn on the revenue side in 2026 (more than double Tikr 2022 estimates of $7.3bn), which at a 30% FCF margin would be ~$5bn of FCF. NOW today trades at a ~$77bn valuation, meaning if the stock goes flat in 2026 and management projections are accurate it would trade at 6.4% FCF yield and likely still be CAGRing FCF at low teens (for the next few years the guidance for revenue is 20%+ and for FCF could be higher w/ operating leverage).

Given the stability of NOW’s cash flows and future growth, this seems way more attractive than the 10y when both basically trade 25x FCF today.

Attractive Current Yield v. 10y, Stable Cash Flows / Possible Growth or Limited Decline Ahead

There’s another attractive set of opportunities for equities with FCF yields double or more than the 10y where cash flows are locked in for several years into the future and “coupons” should be stable (growing or slightly shrinking) into the future. TRTN 0.00%↑ has appeared a lot in this blog and the pitch at this point I'm sure is getting old - the company has leases locked in 10+ years into the future and lessee credit risk doesn't concern me, as even during 2008-9 and the industrial recession of 15-16 nearly all major lessees kept paying for containers.

TRTN telegraphed in 2021 they would spend most of 2022 pumping the brakes on new container purchases and buying back stock instead. They’ve done exactly that and bought back 3.9m shares YTD, or 6% of the float (remember that 5 more months of the year are left from when they reported). At the current price the dividend is 4.7% and likely to increase. They are well below their historical payout ratio and have a long record of raising the dividend. This year will be a 10%+ return of capital to shareholders and future years should play out similarly.

I do think EPS could shrink slightly in a multi year recession as it’s unlikely we ever see the extraordinary leasing environment of 2021 again (meaning smaller gains on sale from containers and new leases with possibly worse economics than leases they’re replacing), but:

The company will get bigger when a normal leasing environment returns, using FCF to buy more containers and then lease them out

Share buybacks will keep boosting EPS

TRTN right now is a double digit plus FCF yield and I have conviction at the current price it continues yielding double the ten year and has forever duration, going back to the original topic of this post.

Other “stable stream of cash flow in leasing / loan origination” equities with limited growth prospects during the recession also are producing 10%+ dividends / FCF yields, albeit some with more leverage than TRTN and/or in industries where the lessees are less safe.

All that said, I think for the TRTNs of the world you can haircut FCF today and still get a forever yield that is 8%+, or double the 10y treasury. Again, why would I buy the 10y when I can get double the coupon and just maybe growth through buybacks / return of a bull market in the future?

For the stocks versus bonds argument, I’m not even saying you have to take a forever time horizon. If you simply take 10 years and look at whether the 10y or equities will produce more free cash flow per price, it seems likely stocks are the winner through today’s high yield, growth, or a combination of both. Ten years takes us to 2032. I am almost certain we see rates drop during that time (markets still have a future rate cut sometime in 2023, so seems like I have 9 years of buffer) and at least one bull market.