Thinking through equity v. corp. bonds opportunity

Risk-reward is getting interesting (Boyd's, Bath & Body, NCMI)

If you read my May post on now being the best buying opportunity since 2020 (I think buying opportunity has become even better), you know I like stock valuations right now. What has become interesting recently is inflation fears - which now seem to be dying down as oil and commodity prices have plummeted - have led to some opportunities to lock in 10%+ bond returns for years.

Interestingly, if you believe expected stock returns are (10y treaury + equity risk premium), this is about what the market is expecting, per this tweet / retweet from Aswath Damodaran and Michael Mauboussin:

This potential return is making me consider increasing my allocation to bonds, along with a few other factors:

For near-term maturities where I think the underlying companies will refinance or pay off the debt, I get the benefit of price going to par. Getting your money back is in some ways a disadvantage (taxes, now have to re-allocate), but I will look past that if my hurdle rate is met and I think there are opportunities to invest after

Longer-term maturities have greater sensitivity to interest rates, so if we see the Fed reverse course on rates, these bonds will appreciate in price. While I’m not a macro expert, I am a contrarian, and I love taking the other side of the popular belief that rates are going to increase for years

There are some key disadvantages here for bonds v. stocks worth mentioning (and note this pros / cons list is far from complete):

Tax consequences for bonds matter. Corporate bond interest payments (yes, not munis) are generally subject to income tax

Bid / ask for less liquid bonds can often be worse than microcaps - during peak COVID, I remember seeing 10+ point spreads (this is on 100 of par value) for some bonds that prior to it had traded at less than a point on bid-ask. When capital markets freeze, there may be no bid

If the bonds do well, the equity will IMO likely do better, although not always (ex. if you have a 10 year bond that yields 20%/y to maturity, the company will have to perform unbelievably to see 20% CAGR on the equity - the bonds are telling you there’s substantial risk to owning the equity)

With these caveats out of the way, I still think the mental model of thinking of bonds as selling a put option on a company and stocks as call options is good. Bonds have capped upside, just like selling a put:

There is some range of outcomes where the bonds will outperform the equity of the same company because debt is paid before equity, and same larger range where equity outperforms because debt is capped and equity value can be potentially infinite.

An extreme example - let’s say for Company X the market believed there was an 100% chance all cash flows and liquidated assets (which come off as cash flows) from a company into infinity could pay the debt but nothing would be leftover. The stock would trade at $0, but the bonds would be paid in full.

I have a friend who often says things like “if you re-created the company at what the bonds are pricing in…”. This is a useful way of thinking about companies that have had their bonds severely haircut relative to par. If you have a company with $100 of debt and the bonds now trade at $0.50 on the dollar and you think they can do $20 of EBITDA, the company is 5x levered currently and 2.5x levered if you “re-created” the company by wiping out the current debt and replacing it with the current-priced equivalent. If you think 2.5x leverage is pretty conservative and EBITDA can increase, there’s maybe a case the bonds are mispriced (note - interest rates are a huge determinant here I’m not discussing - assume in this example rates don’t change so I’m just talking about credit risk and a near-term maturity).

Okay, onto examples. A few companies I’ve recommended on this blog - BYD, BBWI 0.00%↑ , NCMI 0.00%↑ - all trade at 6%+ yields. Reminder - these are all high yield (junk bond) issuers and as the name implies, there’s considerable risk to owning, so do your own diligence.

BYD (Boyd Gaming)

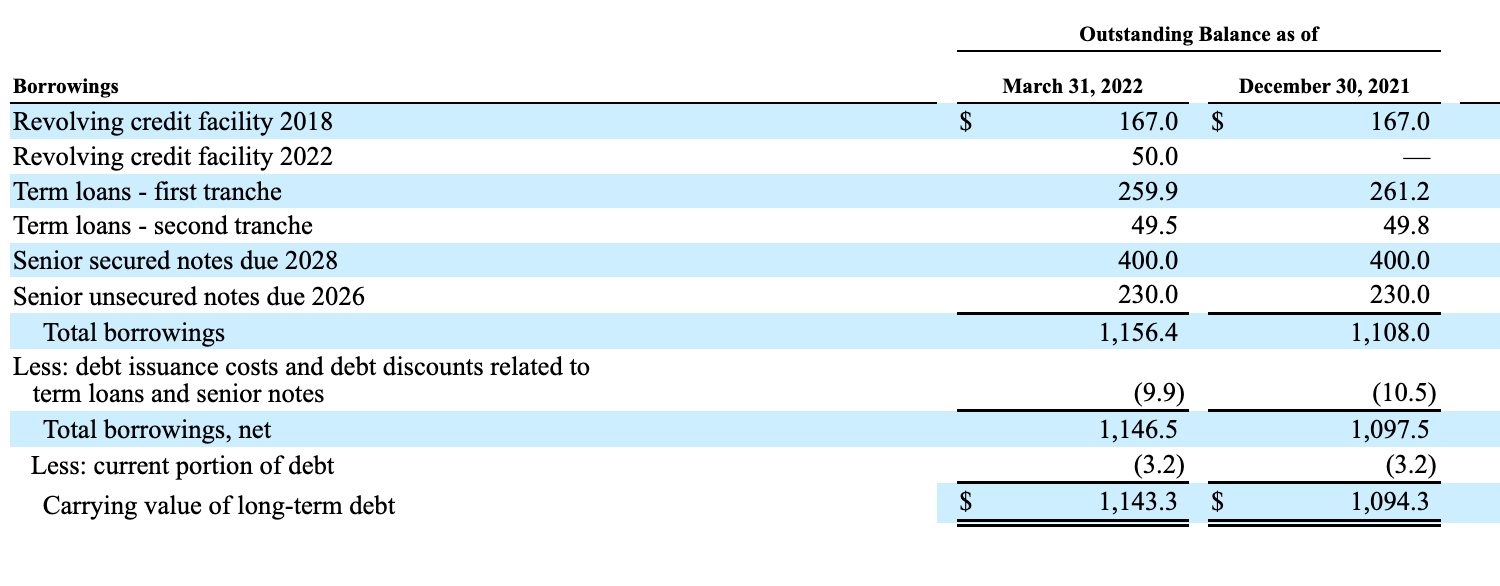

Outstanding Debt

Let’s start with the lowest yield and most conservative pick. Credit to Jeffrey Kamys for pitching Boyd’s equity both times he has been on my podcast, as that is how I originally learned about the company. Leverage is the most conservative (per Tikr, estimated $1.2bn in EBITDA, so ~2.5x levered on LT debt). The company also has been actively buying back shares ($131.8m worth last quarter), pays a small dividend and has $5.4bn of market cap right now. It would take a lot to eat through that equity and take a loss on the bonds.

BBWI (Bath and Bodyworks)

Outstanding Debt

BBWI 0.00%↑ equity has been my worst performer this year alongside NCMI 0.00%↑ - I covered a few posts ago my terrible timing on retail and why I think we’re seeing the sell-off we are. That said, the company from a credit perspective remains IMO fine and is projected to do $1.8bn in EBITDA per Tikr (~2.7x levered through LT debt). I’ve written about the aggressive buybacks before ($1.2bn buyback last quarter) and they also pay a dividend (small - $48m/q). There’s $6.3bn in equity value sitting in front of you, and the company has real assets that could be monetized in a liquidation scenario ($820m, in inventories, $1bn in PP&E):

I’d take a 10% return on stocks and I’ll definitely take it on the bonds of a company I really like.

NCMI (National CineMedia)

Outstanding Debt

Man, it is scary looking at a company with $1bn+ of debt that burned cash last year and sits on an $80m equity stub. The company also has the $217m of revolver debt coming due next year, which at the last conference they spoke at is the primary focus of the CFO (and the reason the dividend was slashed)1. Clearly, NCMI has the worst leverage and debt load of any of these three companies and that is causing a ton of fear with the capital markets mostly shut down right now.

That fear is my best theory on why NCMI has lost 3/4 of its value YTD and the 2026 unsecured now trades at <$0.50 on the dollar. That said, you’ve all heard me share the S&P report that upgraded the company and has them at <5x leverage by end of next year (here it is again).

NCMI isn’t burning cash anymore and is about to report its best quarter since the onset of the pandemic, where it will likely due $20m+ in OIBDA and benefit from the record June box office attendance. They’re selling individual ads for $5-$8m with their platinum offering at the high margins of an advertising business.

If the historic success of Top Gun 2 wasn’t enough, Minions and Thor followed it up with some spectacular performances of their own. Tikr projections suggest to me the next two years alone will produce ~$300m+ in EBITDA, and I’d think the next 10 years has $1bn+ of cash flowing to the debt (recall they did 10 years of $200m in EBITDA prior to COVID). Barring another COVID (I personally think the risk of streaming killing theaters is officially over - in fact, the reverse seems more likely), I am struggling to find reasons why bondholders don’t get paid back here. I’ll also call out that the theater owners (AMC, CNK, Regal, Harkins) all benefit from NCMI existing - the point of this business is to pay out all cashflows to shareholders.

Finally, the company on 6/3 spoke at a conference and the commentary again was more of the same - all demos are coming back to theaters and 2022 is shaping up to 70%+ of 2019. 2023 is looking even better - per the CEO:

As it relates to next year, which is probably the most pivotal year in the movie business, '23, I think it could be -- again, there's a bit of a spread in terms of all of the forecasts that are out there, anywhere from 80% of 2019 to 105%. I'm not going to give you a -- like actual guidance, but I think 80% is conservative.

My thought process at this point - is the better risk / reward owning the bonds if my hurdle rate is 10%? It’s extremely tempting to me to want to lock in a large portion of my portfolio at this yield with better downside protection than equities.

The flip side - if COVID or previous recessions are any indicators, some of the beaten down stocks at their lows are 10x+ baggers and could return well above the yields I cited. Everyone likes their book, but all their names I discussed I believe on the equity side could double and still be conservatively valued. So if I think I have a decent shot at an 100% or even 50% return if it takes two years, why would I settle for 10%?

Another point to argue myself here is some names I’ve pitched on this blog like Triton have double digit free cash flow yields and are giving you close to 10% in buybacks and dividends combined. In theory, I’ll take a forever bond where cash flows are 10%+ to the business (assuming those cash flows are allocated well) over a 10% bond that matures in the next few years.

Of course, before doing any of this, I think the easiest bond trade in the world is the risk-free Series I bonds, which will have Uncle Sam pay you ~9%+ annualized for the next few months and possibly more.

The only question on their presentation at a conference was on this. CFO Ronnie Ng seemed to suggest “amend & extend” was likely and this gets kicked out to 2024. That said, I get the fear on an upcoming maturity in the worst capital raising environment in years.